Blog

BlogHead Case

Case studies of your customers’ or clients’ experience not only helps marketing to new clients; existing clients see the follow-up and feedback they can give as good customer service

FinanceWriter received a commissioned from a major global bank to interview some of their trade finance clients. We were asked to write up the clients’ experience of the bank’s services in the form of case studies that the bank planned to use in their marketing.

The bank had requested their clients put forward someone to speak to FinanceWriter and we conducted interviews with clients around the world who had used a range of the bank’s services.

Case content

The case studies covered a wide assortment of sectors, countries and trade finance services. Besides asking interviewees about the quality of the service, FinanceWriter looked at ways the bank’s sector knowledge, technology and the alignment of the bank’s technology with the clients’ systems contributed to the transactions.

The examples in the case studies built an overall picture of what facilities the bank offered in sometimes, highly-specialised services; how processes worked and how the bank integrated with the clients’ systems and requirements.

Feedback on feedback

This blog does not name the bank so it is quite fair to report that its clients were overwhelmingly satisfied with the services offered by the bank in foreign exchange, trade finance, insurance, export credit guarantees and other services mitigating risk and expediting funding for trade deals.

The standard of their service as reported by their clients didn’t altogether surprise the bank – they wouldn’t have embarked on the project without being confident of a positive response from clients.

However, the bank were surprised by the unsolicited comments from their clients during the case study interviews, about how much they appreciated being asked to offer their views through the case studies.

Feedback takes time and effort. That is why many firms rely on an emailed form asking customers for a review of the service the company has received.

The problem is that such feedback usually comes from the self-selecting few who can be bothered to reply or those who have a beef about the service they didn’t get.

Looking at case studies based on interviews in a different way, in the way the bank did, they could be said to have paid for themselves in the positive reaction clients’ gave simply about being asked to contribute.

Through the case studies the bank was able to connect with and engage with those in the front line, those interacting with banks staff and systems; those with first hand experience of the service and the potential pitfalls.

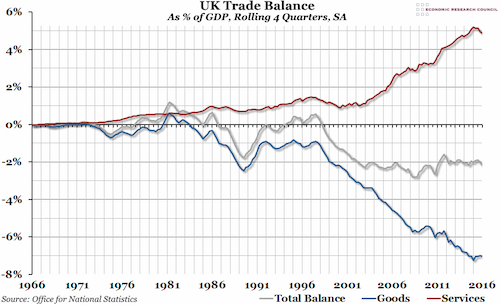

But Britain has a thriving services sector and one that helps to redress the international trade balance of a country where it is too expensive to make things; as the possible demise of its steel industry testifies.

But Britain has a thriving services sector and one that helps to redress the international trade balance of a country where it is too expensive to make things; as the possible demise of its steel industry testifies.